Student Loan Repayment Plans

Standard Repayment Plan

Graduated Repayment Plan

Extended Repayment Plan

Revised Pay As You Earn Repayment Plan (REPAYE)

Pay As You Earn Repayment Plan (PAYE)

Income-Based Repayment Plan (IBR)

Income-Contingent Repayment Plan (ICR)

Income-Sensitive Repayment Plan

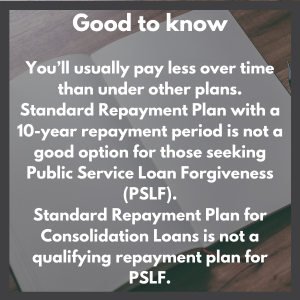

Standard Repayment Plan

Eligible Borrowers

Eligible Borrowers

All borrowers are eligible for this plan.

Monthly Payment and Time Frame

Payments are a fixed amount that ensures your loans are paid off within 10 years (within 10 to 30 years for Consolidation Loans).

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Subsidized and Unsubsidized Federal Stafford Loans

all PLUS loans

all Consolidation Loans (Direct or FFEL)

Read more about the Standard Repayment Plan

Graduated Repayment Plan

Eligible Borrowers

Eligible Borrowers

All borrowers are eligible for this plan.

Monthly Payment and Time Frame

Payments are lower at first and then increase, usually every two years, and are for an amount that will ensure your loans are paid off within 10 years (within 10 to 30 years for Consolidation Loans).

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Subsidized and Unsubsidized Federal Stafford Loans

all PLUS loans

all Consolidation Loans (Direct or FFEL)

Read more about the Graduated Repayment Plan

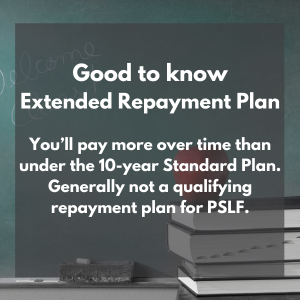

Extended Repayment Plan

Eligible Borrowers

Eligible Borrowers

If you’re a Direct Loan borrower, you must have more than $30,000 in outstanding Direct Loans.

Monthly Payment and Time Frame

Payments may be fixed or graduated, and will ensure that your loans are paid off within 25 years.

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Subsidized and Unsubsidized Federal Stafford Loans

all PLUS loans

all Consolidation Loans (Direct or FFEL)

Read more about the Extended Repayment Plan

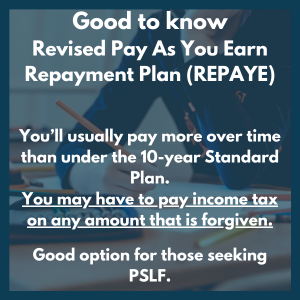

Revised Pay As You Earn Repayment Plan (REPAYE)

Eligible Borrowers

Eligible Borrowers

Any Direct Loan borrower with an eligible loan type may choose this plan.

Monthly Payment and Time Frame

Your monthly payments will be 10 percent of discretionary income.

Payments are recalculated each year and are based on your updated income and family size.

You must update your income and family size each year, even if they haven’t changed.

If you’re married, both your and your spouse’s income or loan debt will be considered, whether taxes are filed jointly or separately (with limited exceptions).

Any outstanding balance on your loan will be forgiven if you haven’t repaid your loan in full after 20 years (if all loans were taken out for undergraduate study) or 25 years (if any loans were taken out for graduate or professional study).

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Direct PLUS Loans made to students

Direct Consolidation Loans that do not include PLUS loans (Direct or FFEL) made to parents

Read more about the Revised Pay As You Earn Repayment Plan (REPAYE)

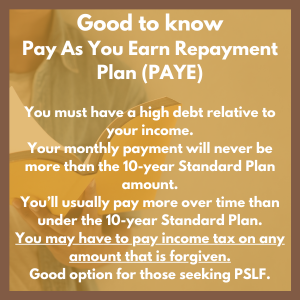

Pay As You Earn Repayment Plan (PAYE)

Eligible Borrowers

Eligible Borrowers

You must be a new borrower on or after Oct. 1, 2007, and must have received a disbursement of a Direct Loan on or after Oct. 1, 2011.

Monthly Payment and Time Frame

Your monthly payments will be 10 percent of discretionary income, but never more than you would have paid under the 10-year Standard Repayment Plan. Payments are recalculated each year and are based on your updated income and family size.

You must update your income and family size each year, even if they haven’t changed.

If you’re married, your spouse’s income or loan debt will be considered only if you file a joint tax return.

Any outstanding balance on your loan will be forgiven if you haven’t repaid your loan in full after 20 years.

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Direct PLUS Loans made to students

Direct Consolidation Loans that do not include PLUS loans (Direct or FFEL) made to parents

Read more about the Pay As You Earn Repayment Plan (PAYE)

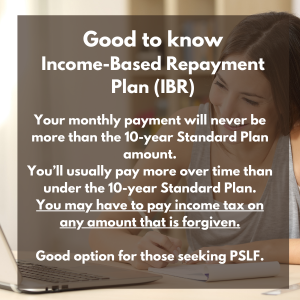

Income-Based Repayment Plan (IBR)

Eligible Borrowers

Eligible Borrowers

You must have a high debt relative to your income.

Monthly Payment and Time Frame

Your monthly payments will be either 10 or 15 percent of discretionary income (depending on when you received your first loans), but never more than you would have paid under the 10-year Standard Repayment Plan.

Payments are recalculated each year and are based on your updated income and family size.

You must update your income and family size each year, even if they haven’t changed.

If you’re married, your spouse’s income or loan debt will be considered only if you file a joint tax return.

Any outstanding balance on your loan will be forgiven if you haven’t repaid your loan in full after 20 years or 25 years, depending on when you received your first loans.

You may have to pay income tax on any amount that is forgiven.

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Subsidized and Unsubsidized Federal Stafford Loans

all PLUS loans made to students

• Consolidation Loans (Direct or FFEL) that do not include PLUS loans (Direct or FFEL) made to parents

Read more about the Income-Based Repayment Plan (IBR)

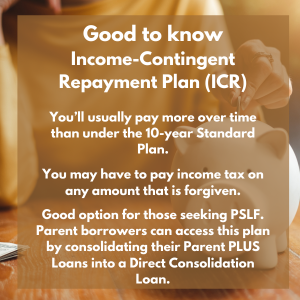

Income-Contingent Repayment Plan (ICR)

Eligible Borrowers

Eligible Borrowers

Any Direct Loan borrower with an eligible loan type may choose this plan.

Monthly Payment and Time Frame

Your monthly payment will be the lesser of

20 percent of discretionary income, or

the amount you would pay on a repayment plan with a fixed payment over 12 years, adjusted according to your income.

Payments are recalculated each year and are based on your updated income, family size, and the total amount of your Direct Loans.

You must update your income and family size each year, even if they haven’t changed.

If you’re married, your spouse’s income or loan debt will be considered only if you file a joint tax return or you choose to repay your Direct Loans jointly with your spouse.

Any outstanding balance will be forgiven if you haven’t repaid your loan in full after 25 years.

Eligible Loans

Direct Subsidized and Unsubsidized Loans

Direct PLUS Loans made to students

Direct Consolidation Loans

Read more about the Income-Contingent Repayment Plan (ICR)

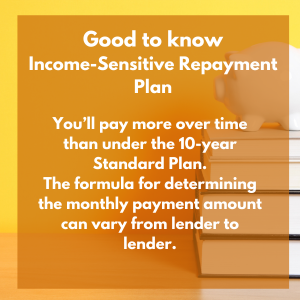

Income-Sensitive Repayment Plan

Eligible Borrowers

Eligible Borrowers

Available only for FFEL Program loans, which are not eligible for PSLF.

Monthly Payment and Time Frame

Your monthly payment is based on annual income, but your loan will be paid in full within 15 years.

Eligible Loans

Subsidized and Unsubsidized Federal Stafford Loans

FFEL PLUS Loans

FFEL Consolidation Loans

Read more about the Income-Sensitive Repayment Plan